Since April, the Chinese television market

has entered the stocking cycle of the 618 promotion season. However, the

shipment volume in April and May showed a year-on-year decline for two

consecutive months. The main reason for this is that the market retail and

inventory status from the end of last year to the first quarter of this year

was not good. Relatively speaking, although overseas markets are experiencing

multiple local wars such as Russia Ukraine and India Pakistan, the markets of

major economies have maintained a relatively low growth rate since the

beginning of this year, providing certain support for the global market.

Overall, the outsourcing strategy of global top TV brands has not undergone

significant changes. The TV OEM market maintained growth in shipments in May.

According to data from RUNTO Technology, within the statistical scope, the

total shipment volume of top 10 professional ODM factories in May 2025

increased by 2.6% compared to the same period last year, but decreased by 2.4%

compared to April. Since the beginning of this year, the OEM market has

achieved five consecutive months of year-on-year growth, but the magnitude is

not significant, both in single digits.

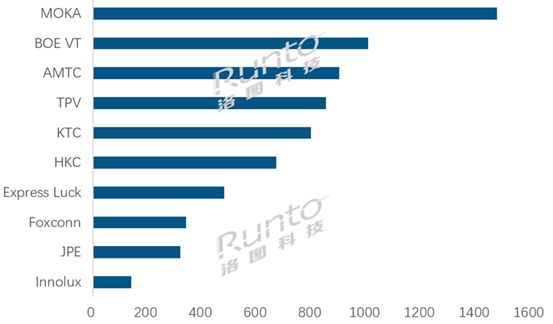

Among the 10 professional factories within

the statistical range, there were fewer increases and more decreases, and a

polarized Matthew effect was observed where the strong remained strong. Among

only four factories that saw an increase, MOKA (Maojia), BOE VT (Video), and

HKC (Huike) all saw growth rates exceeding 10%, while TPV (Crown) was around

5%. The top three have supporting panel resources, while the latter are

traditional old brand factories. --MOKA shipped nearly 1.5 million units in

May, reaching a high point this year and ranking first steadily, with

year-on-year growth of 13.5% and 7.0% respectively. The cumulative shipment

volume in the first five months increased by 12.6% compared to the same period

in 2024, continuing to maintain growth and leading advantages. In addition,

according to the "May Shipment Briefing of Chinese TV Market Brands"

previously released by RUNTO Technology, TCL series brands ranked first in the

Chinese market with a shipment volume of over 600000 units. --BOE VT (Video)

shipped over 1 million units in May, ranking second among professional contract

manufacturers and significantly improving its ranking by 4 places compared to

the previous month; The year-on-year and month on month growth rates are both

around 40%, making it the factory with the largest growth rate for the month.

The core customers are still domestic customers Xiaomi, overseas customers

Vizio and LGE, with a year-on-year growth rate of over 20%. RUNTO Technology

predicts based on industry chain information that the shipment volume of VT in

the second quarter will reach nearly 3 million units, a significant increase of

about 37% compared to the same period last year; If Q2 can be achieved, the

year-on-year increase in cumulative shipments in the first half of the year

will reach 25%. --AMTC (Zhaochi) shipped approximately 900000 units in May,

ranking third among professional contract manufacturers, with both shipment

volume and ranking unchanged from April. The annual cumulative shipment volume

from January to May this year has exceeded 4 million units, with a certain

increase compared to the same period last year. --TPV shipped approximately

850000 units in May, ranking fourth among professional contract manufacturers,

with a slight year-on-year increase of 5.1%. The increase mainly comes from the

self owned brands Philips and AOC, whose combined shipments for the month

increased by 18.4% and 9.6% month on month, respectively. At the same time, the

shipment volume of overseas customer Vizio, as well as domestic customers

Hisense and Skyworth, also showed varying degrees of growth compared to the

same period last month. In addition, the monthly shipment volume of Element,

which started in the second half of last year, has now stabilized at over

100000 units. --KTC (Kangguan) shipped approximately 800000 units in May,

ranking fifth among professional contract manufacturers and basically unchanged

from the same period last year. The cumulative shipment volume from January to

May this year is about 3.8 million units, an increase of 11.5% compared to the

same period last year. --HKC (Huike) shipped approximately 670000 units in May,

ranking sixth among professional contract manufacturers, with a year-on-year

increase of 11.7% and a certain decline compared to April. --Express Luck

shipped approximately 480000 units in May, ranking seventh among professional

contract manufacturers, with a year-on-year decrease of over 20%. --Foxconn and

Innolux ranked eighth and tenth in the professional contract manufacturing

industry with shipments of 340000 and 140000 units, respectively, showing a

significant decrease compared to the same period last year; Especially Innolux

saw a significant year-on-year decline of 30%, ranking among the top in terms

of decline.

Global professional TV ODM factory shipment

ranking in May 2025

Note: The TV ODM ranking does not include

the four self owned factories of Changhong, Konka, Skyworth, and Hisense. RUNTO

believes that the market performance in the future may not be completely

consistent with the months that have already passed this year. In the Chinese

market, this year's 618 shopping festival is a combination of the national

subsidy promotion, astonishing subsidies, and proactive price reductions, with

a predicted final sales increase of over 15%. But by Q4, there will be a

significant decline compared to last year when there was already a national

subsidy. In the overseas market, last year was a sports big year with the

European Cup, Copa America, and Olympic Games gathering, while this year is a

year of tariff storms and frequent local wars, and overall TV demand is

expected to decline. These changes will gradually have an inevitable impact on

the television OEM market.